Stars are aligned for a stellar year

By Charles C. Shinn Jr., PhD

Founder, Builder Partnerships

Housing closed out 2017 very strong. In fact, 2017 is tracking to be the strongest year in the housing recovery. Demand remains high, and most builders will start the year with a strong backlog. Inventory is low for both new and existing homes, and interest rates are still helping with affordability, although that bears watching as the Fed is predicted to raise interest rates three more times in 2018.

Economic conditions

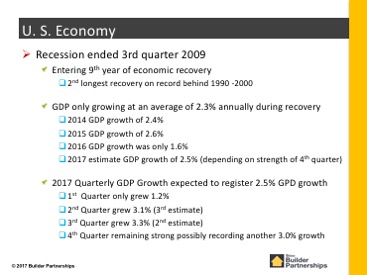

As always, the strength of the housing industry is closely tied to the overall economy and the job market. Officially, the recession ended in the third quarter of 2009, which means we now are entering the ninth year of economic recovery. The gross domestic product (GDP) has been growing at an average of 2.3 percent annually during the recovery; depending on the strength of the fourth quarter, the estimated GDP growth for 2017 is 2.5 percent.

Consumer confidence is strong, as was spending for the holidays. Unemployment, which was 10 percent October 2009, was at 4.1 percent for October and November this year, which is effectively full employment. It’s anticipated to drop to about 3.5 percent during 2018. Average hourly earnings in November increased year over year by 2.5 percent, or about 64 cents.

Housing supply

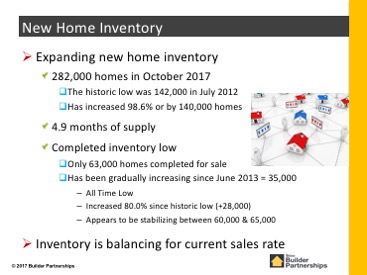

A balanced housing market should have about a five- to six-month supply of new and existing homes. Currently, builders have a 4.9 percent supply of new homes under construction (though not much finished inventory). In the existing home market, the supply is only 3.9 months.

Right now, we have 10 percent fewer existing homes on the market than in 2016. Fifty percent of everything on the market is selling within about 30 days.

This is unusual, and a number of reasons account for it. With prices going up, some home owners are choosing to take out equity lines of credit and remodel their current homes rather than move. Also, people are moving less often. On average, households are moving about every 10 years. In the past, moves were happening about every six years. This could be a holdover from the recession or the fact that there’s so few new and existing houses on the market.

Affordability

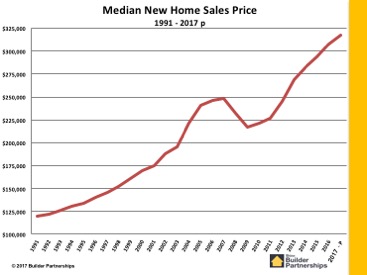

As expected, with demand outstripping supply, prices are increasing. Builders face a shortage of labor and lots and construction costs are escalating. All of this affects affordability.

Housing prices have been going up about 5 percent per year, but wages haven’t gone up anywhere near that. The thing that has helped is that consumers look at monthly payment, and low interest rates have subsidized the ability to raise prices without increasing the monthly payment. If the mortgage interest rate rises to 5 percent, that will knock builders out of the affordable range and the ability to pass along cost increases to consumers.

To address this, I’m seeing builders go back into their inventory and cutting out about 100 square feet to make product more affordable — builders are focusing on homes of 1,600-2,000 sf as opposed to the 2,500-3,200 sf upper-end homes we saw coming out of the recession. It will be more important than ever to keep a tight rein on direct construction costs.

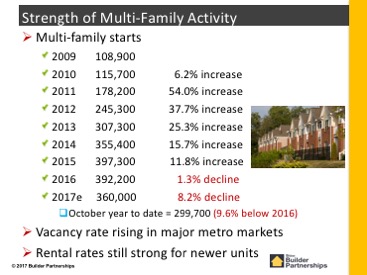

The multifamily market

I’m seeing changes in the multifamily market, which is getting pretty saturated in the major markets. We’re seeing a rise in vacancy rates and a lot of new inventory coming onto the market. There is still room for growth in secondary markets. Expect to see the mix change from rental to condo/townhouse to get the first-time home buyer into the market.

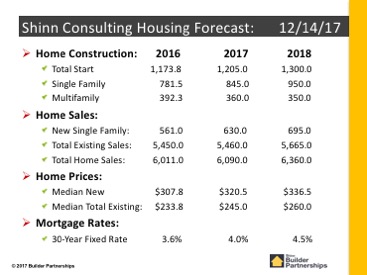

Forecast

My forecast for 2018 is that with significant pent-up demand, increasing household formation, extremely low inventory, relatively low mortgage rates, an easing of credit requirements, and the effective end of foreclosures and short sales, the stars are perfectly aligned for a stellar year.

New home sales and new home construction will continue to expand. Single-family construction will rise 10-12 percent, and new home sales will increase by 10 percent. Existing home sales will probably increase about 3.5-4 percent. Multifamily will likely remain flat to a slight drop.

The median price of new homes should increase about 5 percent to $335,500. For existing homes, expect an increase of about 6 percent to a median price of $260,000.

Lennox Residential is a leading global name in home comfort. Lennox is built on a legacy of innovative firsts, from the introduction of the riveted-st...